Small and Micro Caps Diverging, Defensive Stocks Breaking Out, KO Earnings, Insider Weekly Sales To Buys: 143 To 1

Note: To sign up to be alerted when the morning blog is posted to my website, enter your name and email in the box in the right hand corner titled “New Post Announcements”. That will add you to my AWeber list. Each email from AWeber has a link at the bottom to “Unsubscribe” making it easy to do so should you no longer wish to receive the emails.

Andrew Thrasher beautifully captured the most important technical divergence in the market yesterday (Monday) morning in the above tweet. While the large cap S&P 500 continued to move higher through the end of last week, small caps and micro caps were not confirming the move. This is important because smaller stocks are riskier and so weakness here shows flagging risk appetite.

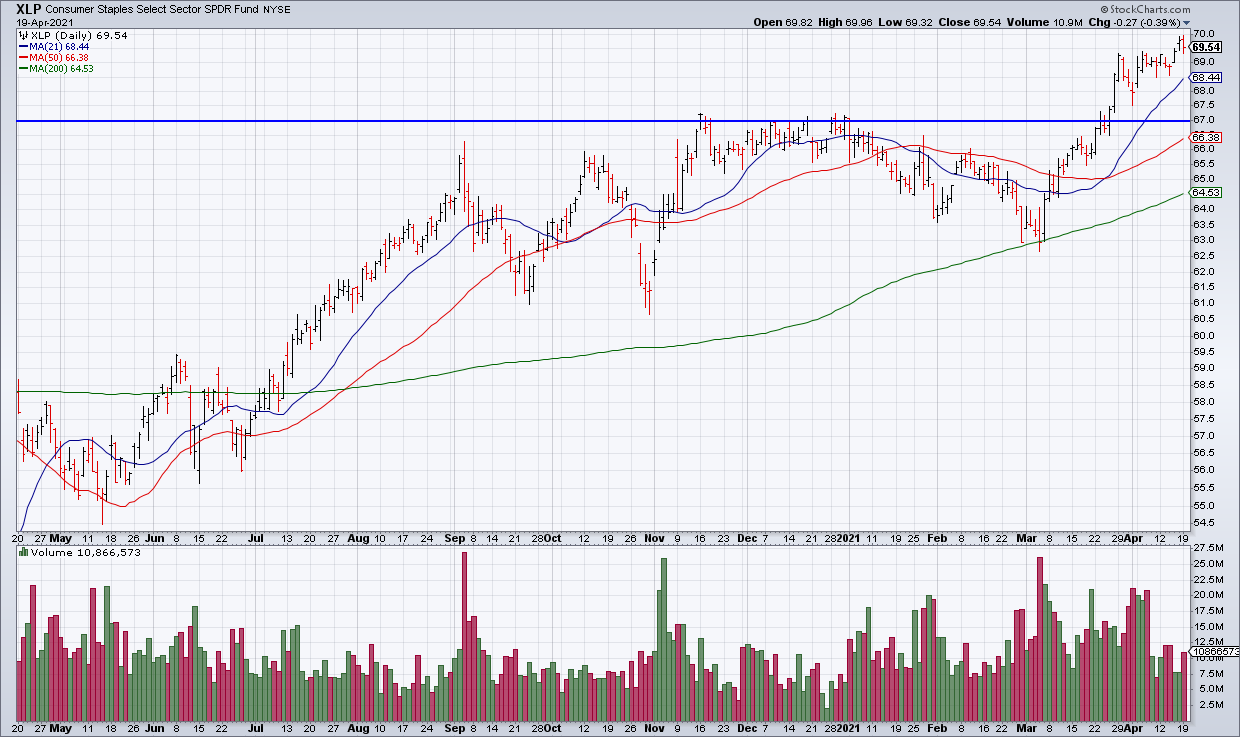

Within the S&P itself, defensive stocks as exemplified by Consumer Staples (XLP) have broken out. The XLP consists of stocks like Procter & Gamble (PG, 16% of the XLP), Coke (KO) and Pepsi (PEP)(19.5% combined), Walmart (WMT) and Costco (COST)(14% combined), and Altria (MO) and Philip Morris (PM)(9% combined). These are the kinds of stocks and businesses that do well in difficult markets and economic conditions, not the kind investors buy when risk appetite is high and they want to play offense. (Top Gun is long PG, WMT, MO and PM).

While Top Gun is long a number of defensive names which are working now, I had to stretch my valuation parameters to buy them. We can get a window into valuation in these types of names via an examination of KO 1Q21 earnings from yesterday morning.

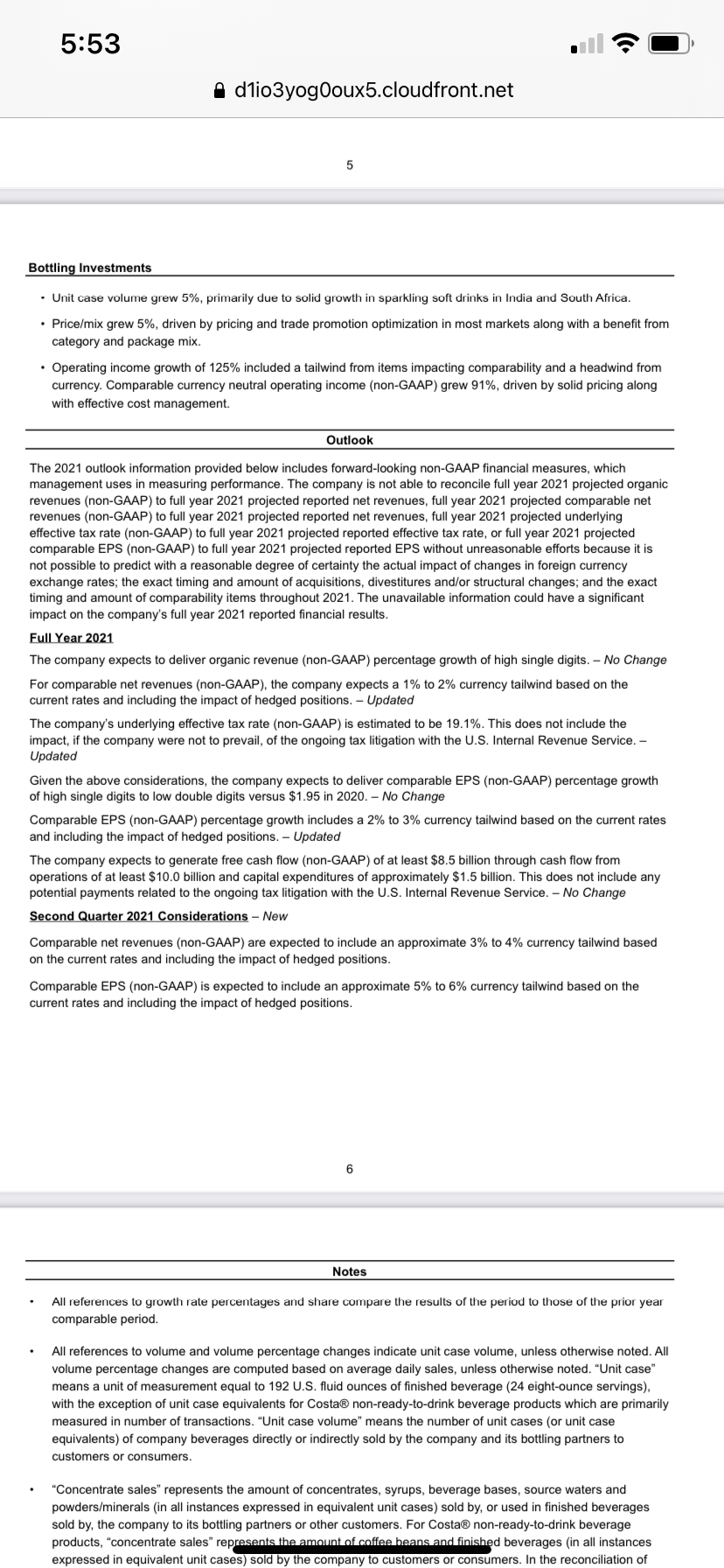

KO reported a strong quarter with Organic Revenue +6% and Non-GAAP EPS of 55 cents compared to 50 cents a year ago. 2021 Guidance looked especially good with the company guiding to Organic Revenue growth in the high single digits and Non-GAAP EPS up high single digits to low double digits from the $1.95 they earned in 2020.

However, while the stock is acting well now and the fundamentals are strong and look to continue to be so, KO is by no means cheap. If we do the math and forecast 2021 Non-GAAP EPS to be +10% to $2.145, we get a forward P/E multiple of 25x. WMT and PG, which I am long, are at similar valuation levels. Nevertheless, I do think this is the place to be in the stock market right now.

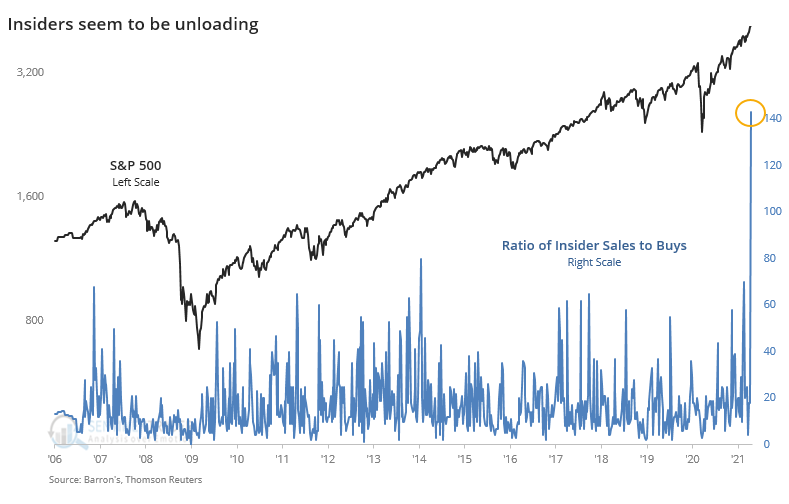

That’s because most of the rest of the market is not overvalued but insanely so! One indication of this is that insiders, who know their businesses better than anybody, bailed last week at an unprecedented 143 to 1 ratio of sales to buys (“Investors go all in as insiders fold” [SUBSCRIPTION REQUIRED], Sentimentrader, April 19). When the smart money gets out, you may want to consider doing so as well.